Laurentian Economics Professor, Dr. David Robinson is Sudbury’s answer to Toronto’s high profile Dr. Richard Florida – the famous American urban theorist who garners media headlines and currently teaches at the University of Toronto. Robinson is recognized as the “Godfather” of Sudbury’s Mining Supply and Services cluster highlighting the importance of this dynamic sector in the early part of the decade. He was instrumental in spearheading the plan for the School of Architecture at Laurentian which is garnering public and political support and continues to help change public policy on a wide variety of economic initiatives affecting Northern Ontario.

Laurentian Economics Professor, Dr. David Robinson is Sudbury’s answer to Toronto’s high profile Dr. Richard Florida – the famous American urban theorist who garners media headlines and currently teaches at the University of Toronto. Robinson is recognized as the “Godfather” of Sudbury’s Mining Supply and Services cluster highlighting the importance of this dynamic sector in the early part of the decade. He was instrumental in spearheading the plan for the School of Architecture at Laurentian which is garnering public and political support and continues to help change public policy on a wide variety of economic initiatives affecting Northern Ontario.

The Institute of Northern Ontario Research and Development (INORD)

Copper Cliff, Ontario

December 4, 2008

HOW I GOT INTO THIS

Let me start by telling how this speech got its title. A few months ago I was asked what I would talk about. We had a stock market commotion going on, a Canadian election underway, and an American election too. So I said I could either use the speech that I used two years ago, or I could wait until the dust settled.

I obviously made the wrong choice. I had no ideas of the interesting and surprising twists that that a parliamentary system can provide. We have a temporary resolution as of 11:45 this morning that seems to tell us the government is likely to abandon the contractionary policies announced last week by Finance Minister Flaherty. The government will be forced to adopt a program much closer to that proposed by the opposition parties that make up the “Coalition.” That is good news for Sudbury, I would argue, and it brings Canadian policy in line with our industrialized partners.

When I came through the door today I had not yet heard of the reorganization announced by the city’s largest employer. Vale confirmed it will close its Copper Cliff South mine for an “undetermined period.” The company’s Voisey’s Bay mine in Newfoundland, which ships nickel to facilities in Sudbury for processing, will be shut down during the entire month of July. The company also put off the development of its Copper Cliff Deep project, deferring the expenditure of $138-million (U.S.) for at least a year.

Vale had announced on Wednesday it is laying off 1,300 workers and putting 5,500 more on paid leave. Layoffs by Vale, one of Brazil’s two leading companies along with state oil company Petrobras are being taken as evidence that emerging markets have not ”decoupled” from the US as some economists hoped.

The announcement comes not long after Xstrata Nickel said it will cease operations at its Craig and Thayer-Lindsley nickel mines ahead of schedule and replace them with the new, lower cost Nickel Rim South and Fraser Morgan mines in Sudbury. The moves were prompted at least in part by slumping nickel prices.

Between the time I left home and now conditions have changed. New information will emerge tomorrow when the Labour Force Survey for mid-November is released. It will almost certainly show large losses in the manufacturing sector in Ontario, largely due to the difficulties in the auto sector.

In any case, the dust hasn’t settled and here I am, standing in front of a very knowledgeable audience trying to answer questions that don’t have answers yet.

Anyone who thought the dust might settle by now probably can’t be trusted to forecast economic developments anyway. I wouldn’t listen to me anymore than I’d listen to, for instance, the famous head of the Federal Reserve Bank in the USA, Allan Greenspan. Greenspan was the world’s most powerful central banker. He was charged with keeping the US economy on track.

He told a business lunch in Toronto on November 7, “I’m not going to forecast where we are going because I frankly don’t have a clue.”

Economists, after all, were put on earth to make weathermen look good.

Economists are pretty good at one kind of prediction – when things are ticking along the majority of us predict they will keep ticking along. If even one big change happens it gets harder. Two big changes, two “shocks,” and we are immediately into uncharted territory. We have had more than two shocks.

It is people who mess up economic models. Especially when they start guessing what other people are thinking. When investors begin to think that profits will drop they cut back on their investing. How do they know profits are about to drop? Other investors say so. What happens when they cut back? They make profits drop for others, and they actually become evidence that investors think profits are going to drop. It’s the mathematics of positive feedback and it can produce wild swings. This was one of the key observations underlying Keynesian economics.

You find more positive feedbacks and more herd behaviour when you look at the banking system. Banks fail because bankers won’t even lend to each other. One of the main purposes of banking reserves and financial sector regulation is to prevent runs on the banks. In 1929 the US had roughly 24,000 banks. By 1933 it had 12,000. These failures contributed greatly to the length of the Great Depression according some theorists. We are seeing the equivalent of bank failures and massive consolidation in the financial sector today. A run on a hedge fund is really no different than a run on a small-town bank in 1930.

A shortage of liquidity appears to have been the reason for the bank failures after the 1929 stock market crash. There is now seven hundred billion dollars’ worth of evidence that policy makers2 have learned some lessons and are prepared to act with unprecedented speed. This rapid action, combined with the equally unprecedented coordinated actions of the central banks and Finance Ministries of the industrialized nations suggests that we should not be expecting the financial crisis to propagate to the real economy as it did in the 1930s. Even without the bailouts the link between the paper-trading economy and the “real” economy has been weakening over the last 30 years.

On the other hand new sources of instability have become prominent. Even ordinary people can contribute to the confusion and panic behaviour today. The Conference Board Consumer Confidence Index, which had declined to an all-time low in October, improved moderately in November in the USA, but in Canada it reached a 26-year low. There is real fear that low consumer confidence will result in reduced spending, removing money from the circular flow of the economy and amplifying the effects of other withdrawals.

Some very grim predictions are being passed around by some pretty serious sounding people. Nial Ferguson, historian and author of the 2008 book, The Ascent of Money, is predicting a recession that ranges from two years to a lost decade. Ferguson claims that the model for the current crisis is the Japanese collapse of the 1990s.

Richard Koo, Chief Economist for Japan’s Nomura Research Insititute, on the other hand, says that Japan did not lose a decade as Ferguson claims. Koo was an economist with the US Federal Reserve Bank of New York (1981-84) and a Doctoral Fellow of the Board of Governors of the Federal Reserve System (1979-81). He is the first non-Japanese to be involved in developing Japan’s five-year economic plan. For nearly a decade he has been voted as one of the most reliable economists by Japanese capital and financial market participants.

According to Koo in The Holy Grail of Economics: Lessons from Japan’s Great Recession, Japan maintained the real economy in the face of a financial collapse by spending heavily to maintain the real economy. It ran up debt and spent a decade working through the effects of a bursting banking bubble, but the Japanese economy achieved fairly steady growth through the period. Growth was maintained, in fact, during a period of zero population growth that would normally result in a decline in growth.

Koo describes Japan’s problem as “balance sheet recession.” Imaginary asset value disappears as a result of a bubble bursting. It takes time for firms to write down all the imaginary losses. They don’t start spending again until they clear the books and regain their confidence.

Even if Koo is right that the problem is simply the time required to get over the vanishing of imaginary wealth, we still need to ask where we go from here.

The popular press has become attached to dramatic bad news: good news tends to get buried. For example, media reports about the sharp rise in house sales in September to the highest level in a year got only a fraction of the exposure given to the bad news stories. In most cases, the good news was qualified by news that the value of houses had dropped over the past year. We all know that house prices have declined sharply over the past year, but news that activity in the housing market had picked up in the month was significant. And is it bad news if housing gets more affordable?

The negative reporting has created a downward spiral that feeds on itself, setting up the danger of a self-fulfilling prophesy as consumers cut back on spending and business owners start cutting employees on the basis of what might come to pass.

With so much going on there are many different views about what will happen. I found a Russian joke that pretty much sums up our problem:

“Ivan and Boris are taking a break from a long summit, Boris says to Ivan, “Ivan, Ivan, you know, I have a big problem I don’t know what to do about. I have a hundred bodyguards. I have discovered that one of them is a traitor, but I just don’t know which one!”

“Not a big deal Boris”, says Ivan, “I’m stuck with a hundred economists, and only one of them tells the truth. And it’s never the same one.”

You can decide if I am the one telling the truth today. Here are the main topics I want to touch on:

(1) Mining economy

(2) Politics and economics: Canada and the world

(3) Opportunities and dangers

The general question is this: Sudbury is doing well. Will this world recession set us back to where we were in 2000?

The general answer is, I think, that Sudbury will feel this recession, and the pain will fall on some more than others, but the set-back is likely to be shorter and shallower for Sudbury than for the rest of the country. The challenge for the City of Sudbury is to come out of the trough stronger than we go in.

THE MINING ECONOMY

We might expect Sudbury to be especially hard hit when the economy dips. The resource sector generally exaggerates the movements of the general economy. Our short hand phrase for this tendency is the “Boom-Bust” cycle. Let me try to explain why I think that Sudbury will be less affected in this particular downcycle than most of the country.

Sudbury relies on both current production and on the development of new mines.

Direct employment in mining is supplemented by indirect employment as the Mining Supply & Service (MS&S) sector supplies consumables for production as well as equipment and material for mine development.

There are a strong of signs from the mining industry that the major miners are not expecting a major recession at this point. The latest issue of International Mining Project News (released December 5) includes news received within the past two weeks of no less than 20 prefeasibility studies, 18 feasibility studies and 32 projects in development, plus mines coming into roduction, expansions and more.

Examples include:

(1) Mitsubishi Materials Corp. advancing $28.75 million on Tuesday to Similico Mines Ltd., a subsidiary of Vancouver’s Copper Mountain Mining Corp. (CMMC), to assist in the redevelopment of a copper mine near Princeton, B.C.

(2) Osisko Mining seeking funding for a gold project in Malartic, Quebec.

(3) El Morro SCM has proceeding to the Environmental Impact Study (EIS) for its $2.5 billion ElMorro copper project to the Environment Commission (CONAMA) for the Region of Atacama, Chile.

(4) EMED Mining expanding the project life and production level for Proyecto Rio Tinto (PRT) mine it is restarting. Further expansion is expected after production is underway.

(5) Commissioning of the gold production facility in the Molejon gold deposit in central Panama

(6) BHP Billiton announcing it will increase installed capacity across the company’s Western Australia iron ore operations by 50 Mt/y to 205 Mt/y. New production is scheduled for late 2011.

(7) Ausmelt winning a new contract in Bulgaria, covering second Ausmelt furnace as part of the lead smelter modernisation. The company has also signed a Licensing Agreement with Korea Zinc Co. Ltd for the construction of two new Top Submerged Lance (TSL) technology furnaces for lead smelting.

(8) Kinross Gold expanding its pipeline of producible ore by acquiring Minera Santa Rosa SCM for $250 million.

It is possible that the decision yesterday by Vale to move some 5000 workers to paid leave status rather than layoff status should be seen as a sign that the company expects to need those workers fairly soon.

According to Lawrence Roulston, a geologist and mining analyst, the major mining companies, whether precious or base metal, are still producing at or near capacity. Deposits are being steadily depleted, so undeveloped metal deposits will continue to have enormous value, even if that value is not reflected in the share prices at this moment.

Caterpillar Chief Executive James Owens said last week in Washington that he is convinced that the long-term demand for minerals will ”grow substantially because China, India, Southeast Asia, Latin America, all these emerging countries can’t grow without minerals.” Caterpillar has a strong order backlog from the mining industry, although other firms are reporting some cancellations. The very large Chinese stimulus package announced recently will help to maintain Chinese demand. China has little room politically to allow income growth to decline, in fact, which is encouraging for our markets.

The energy sector is related to mining and is a growing market for Sudbury’s Mining Supply and Service (MS&S) sector. While oil prices have fallen and oil company shares are down, U.S. oil consumption, on a per capita basis, is still 25 barrels a year. In Japan, the figure is 14. The Chinese use only two barrels per person per year, only 8% of the U.S. consumption level. The figure for India is even lower, at 0.8, 3% of the U.S. level. The low levels in developing countries will rise faster than levels in developed countries can possibly fall as a result of conservation policies. Rising energy demand will push prices up again fairly soon.

In the Supply and Services sector in Sudbury, local business people are reasonably confident despite contract cancellations and worrying news. Kevin Costante, Deputy Minister of Northern Development and Mines told SAMSSA member at their Annual General Meeting last week that “the government has a vision of the supply and services sector being a key part of building a sustainable mining industry.” he went on to say “In our view” he said, ”SAMSSA is working effectively to build capacity and increasing international recognition and capabilities of its members…. We look forward to working with SAMSSA and Greater Sudbury in marketing the mining services and supply sector to the world.”

This recognition is an important step toward having the Sudbury MS&S sector recognized as a national treasure.

The Statistics Canada Labour Force Survey showed Sudbury with an unemployment rate below that of the province as a whole, an unusual state of affairs. Furthermore, the national rates were well below the 30-year average, although a sharp increase is underway. This is more evidence that a serious recession has not yet taken hold despite the fact that the financial crisis in the USA has been underway for more than a year and a half.

Overall the news for the mining sector is remarkably positive, given the talk about depression and crisis.

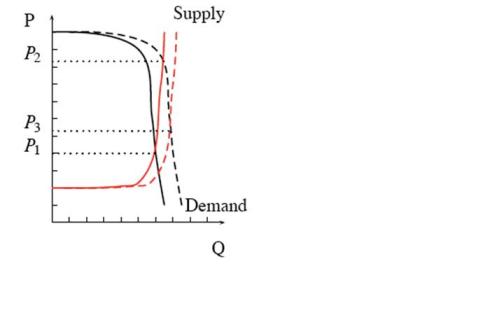

It is important to understand why this might be so. Here is where a bit of economic theory might help. There are good theoretical reasons for thinking Sudbury is relatively insulated. Consider direct demand and supply for a typical metal.

2.1. The nature of demand.

In Figure 1 a stylized version of a metal market is shown. Both Supply and Demand are very steep. Supply is steep because the number of mines and ore-bodies is limited and new mines take time to bring on-line. Supply is capacity constrained. In this situation a relatively small outward shift in demand outward to the dashed line leads to a very large increase in prices, exactly the situation that we have observed.

The increase in demand was largely due to rapid development in the BRIC countries, Brazil, Russia, India and China. To the extent that the price increase is expected to continue, it is capitalized into share prices, so the rise in price is associated with a rise in share prices. As capacity grows due to investment, the price should fall again. The drop in price from P2 to P3 leads to a reduction in the return to the mines and to a drop in share prices. The rise in share prices makes imaginary wealth disappear, causing concern among investors. Since the long-run trend in demand is outward, we expect a general ratcheting of the supply curve outward, accompanied by a series of price fluctuations.

A very similar process happened in the housing market. NO real houses disappeared, so real housing wealth did not change, but the book value of homes did, and it is the book value that bankers look at.

Supply response is not the only source of instability in imaginary wealth stocks. If demand declines even a small amount prices can fall precipitously. The result is wide fluctuations in metal prices and share prices that signal only small changes in demand or supply.

The decline in nickel prices so far has had very little effect on employment in Sudbury. The bulk of Sudbury’s production is in the relatively flat part of the supply curve. A few of the smaller, newer or older mines are in the upward section of the supply curve, but Sudbury is a relatively low-cost producer. The small, high-cost mines are retired or closed when prices fall. Some may open again if prices rise enough. Most of Sudbury’s production should be stable if the current recession is not too deep or prolonged. The decline in prices has eliminated nickel bonuses. This will reduce spending in the community especially on optional purchases.

2.2. Mine Development.

Producing mines are a moving target – as ore is removed production moves into new areas, production and development are combined. There is, nonetheless, a useful distinction between production and development, including exploration, testing, feasibility studies and preparation of the operating mine. Local mine employees are engaged in both production and on development.

The economics of development projects is different from the economics of production. A look at any mine-planning textbook will turn up a cost-revenue timing diagram like Figure 2. The development period may be 6-15 years. The justification for a project is the price expected during the production period. If a recession (the grey bar) were to occur during the development phase there is no reason to change plans unless the recession changes the expected future price OR for some reason cash flow or financing becomes a problem.

For Sudbury this view of project development is encouraging because mine development should not be affected much by a recession that is expected to be brief. In practice, cash flow problems and unfounded fears do lead to project delays that may be economically irrational. These effects are likely to be minor in this business cycle for two reasons. There is a good deal of confidence in the long run prospects, and the world is still awash in money. Furthermore, interest rates are low, reducing the cost of development.

2.3. New Keynesianism.

In the background we still have the ”financial crisis” and the threat of recession or depression. The concept at the heart of the discussion is “contagion”: will the enormous fluctuation in asset prices and the panic behaviour in the financial sector spill over to the real economy? Keynesianism was really nothing more than the idea that governments can and should prevent the mental problems of the financial sector from infecting the real world. The politics of Keynesianism were that unless governments guaranteed employment they would fall. Today even the bankers in Toronto are calling for counter-cyclical spending by the government – for the Federal and Provincial Governments to run deficits.

They are not alone. On November 9, 2008, Sao Paulo, Brazil, G20 Finance Ministers and Central Bank Governors, noting that “ Some countries are also considering additional fiscal measures to stimulate the economy,” agreed that “countries must use all their policy flexibility consistent with their circumstances, to support sustainable growth” The statement actually hides the fact that only the US and Canadian delegations opposed a call for active fiscal policy.

The election of Barrak Obama in the USA has shifted the balance significantly, however, and Canada stands out as the most reluctant to join the industrialized world in a common strategy.

The enthusiasm for expansionary spending represents a remarkable comeback for Keynesian economic theory. A year ago the word Keynesian was used pretty much the way the Americans us the word “liberal” as a synonym for “immoral socialist”. Policy makers and most economists seemed to have completely forgotten the fact that the approach has worked in the past and is likely to work in the future if applied properly.

Suddenly even many conservative economists are spouting pure Keynesian economics. In fact you can find some pretty standard Marxist stories in the press – even the business press. Economists seem to be very willing to forget and then forget that they forgot Keynesian

techniques, which explains another economist joke.

Q. Why does Treasury only have 10 minutes for morning tea?

A. If they had any longer, they would need to re-train all the economists.

ECONOMICS AND POLITICS IN CANADA

Politics will matter to Sudbury in 2009 as we work our way through the difficulties brought on by the Americans. Politics will directly affect the local economy through whatever expansionary or contractionary policies the senior governments undertake.

At the Federal level we have two guys driving (Harper and Dion) Canadian economic policy who in my view don’t really know what they are doing. These two have made serious mistakes already, they have lied about economic policy, and they are right now trying to deflect attention from a colossal economic blunder. This is strong language, but necessary if we are to understand the political risk Sudbury faces at this point.

Our Prime Minister is regularly described in the press as an economist, and he has strong views on how the economy should be run. In fact Harper has an M.A. in economics, normally just enough economics training to work as research assistant to much better trained professionals. On the basis of his deep knowledge he has repeatedly misrepresented the economic situation and he has repeatedly ignored the advice of the country’s best know economists. A little knowledge is a dangerous thing, it seems.

Jim Flaherty was lawyer before becoming an expert on macro policy and world economics – he was a senior partner in a firm specializing in motor vehicle accident and personal injury litigation. He has been a financial expert since he was appointed Finance Minister of Ontario by Mike Harris on February 8, 2001. Before that he was Solicitor General for the province.

Flaherty was seen as one of the most right-wing figures in the Harris administration. Ernie Eves demoted him on April 15, 2002, to the less-prominent position of Minister of Enterprise, Opportunity and Innovation. That is a total of 14 months and one week of experience. Even so, Flaherty was the second most experienced economics expert in the Conservative caucus. (Liberal defector David Emerson was much better qualified for the post.)

On February 6, 2006, Flaherty became Stephen Harper’s Minister of Finance. It is impossible to predict what this pair will do. They are pretending that their past policies are right. They are heading in a direction contrary to that of almost the entire OECD. They are claiming they will run a surplus when almost every economist is saying they cannot avoid a deficit and they have been changing the story they tell almost every week.

Andrew Coyne, the editor of Maclean’s, and a conservative himself, described the situation this way: “Harper has gone from denying any possibility of a deficit during the election to conceding, post-election, that it was indeed possible, to warning it was probable, to shrugging it off as unavoidable in the circumstances. But all of that was only prologue. Under fire from the opposition who suggested that it was not the economy but his government’s extravagant spending that was to blame, Harper went one step further at last week’s APEC summit in Peru. No longer was the deficit an unpleasant consequence of an economic downturn. Rather it was an “essential” element in fighting it. What was once a bug is now a feature.”

In last Thursday’s Globe and Mail, Lawrence Martin called Harper’s APEC speech “an abrupt and somewhat embarrassing turnabout.”

Few have noticed that, even while he was apparently converting to international Keynesianism, Harper was virtually quoting Milton Friedman on the causes of the Great Depression. It looks suspiciously as though he did his research by re-reading an interview Friedman gave for PBS.

In any case, Harper did call on governments to increase spending. This dramatic turn was exactly what most of the other leaders of the OECD had been asking for. It was also Economics 101, of course. If Harper were to adopt a policy on the scale that his international partners were looking for – including the Americans under Obama, Harper would have proposed a deficit figure in the range of $30 billion – perhaps 2% of the Gross National Product.

The following week – last week – Flaherty announced that the government had already taken serious steps when it cut the GST two years ago and that he planned to run a small SURPLUS for the coming year. Economist immediately recognized this as a commitment to run a contractionary fiscal policy in 2009. The proposal was exactly the opposite of what our allies around the world were asking us to do. It amounted to saying to our friends, “You spend money getting us out of the ditch. We Canadians will sit in the car and enjoy the ride.” Flaherty also announced that under the banner of avoiding a deficit he would attack the public sector unions, limit the payments for pay-equity infringements, and withdraw funds from political parties.

If Flaherty had proposed to significantly expand spending on infrastructure beginning in December and going on through to September, I was going to tell you that the recession for Sudbury was likely to be pretty minor.

After the Economic Update I was going to tell you that the recession in Canada was going to be at least a year longer than I had originally forecast. Given Flaherty’s speech I started to rewrite my predictions.

Then we had a revolution in parliament. I now believe that the Federal government will in fact run an expansionary policy. It will be the policy of the opposition, in fact. Harper and Flaherty will do almost anything to keep power a little longer. They will probably attempt to drag their feet, proposing as little stimulus as they can get away with, delaying the implementation and choosing projects that are as transitory as possible, but even a bad program will moderate the effect of the recession in the USA.

LOOKING AHEAD

Here is another take on what to expect from an economist: A mathematician, a statistician and an economist apply for the job of Deputy Finance Minister in the Federal government. Ontario’s own Jim Flaherty interviews each of the candidates.

He starts with the mathematician, thinking that mathematicians are especially good with complicated questions. He asks, “What do two plus two equal?” The mathematician replies four.” The Minister wants to test his confidence, since showing confidence is so important for politicians, so he asks “Four, exactly?” The mathematician looks at the interviewer incredulously and says, “Yes, four, exactly.”

Jim calls in the statistician and asks the same question. “What do two plus two equal?” The statistician says, “On average, four – give or take ten percent, but on average, four.” This seems pretty promising but he goes on to pose the same question to the economist, “What do two plus two equal?” The economist gets up, locks the door, closes the shade, sits down next to Flaherty and says “What do you want it to equal?”

There is a message in this for us, it seems to me. You asked me to tell you what the future of Sudbury will be. I’d like you to ask yourselves what you want it to be. There will be hard times for some businesses and some families in Sudbury. I hope we will find ways to help. We don’t have much choice about these difficulties, although, as I have said, they will probably be less serious than for most communities. We do have something to say about whether we abandon the very progressive projects we have underway or push even harder for them.

We have had some remarkable successes in the last few years. Creating SAMSSA, building CEMI, and the Living with Lakes Center, which just won an international environmental design contest. NORCAT is scheduled to begin moving operation to its new 60,000sq/ft facility tomorrow.

The Xstrata Nickel Sustainable Energy Centre is underway. The plan to make Sudbury the education center for Northern Ontario is proceeding well. We now have a School of Medicine, and a new School of Education, and will probably soon have a School of Architecture. We have added graduate programs and Laurentian, due largely to an initiative that began off campus, is working on MA in Resource-Based Economic Development. These projects not only contribute to the economy – the School of Architecture is an export industry in its own right – but they add to the capacities of the region.

The School of Architecture will raise the design capacity of local industries eventually, contributing to the regions export capacity. The new MA will increase our capacity to analyze the region’s economic problems and promote solutions that fit Northern Ontario.

There are other projects on the table as well. The Performing arts Center may not fly in its current configuration, but its supporters have made that case that it will be part of our future somehow. There is a movement developing to dust off the plans to redevelop the downtown rail-lands.

There are economic problems coming, at least for a short while, but all of these projects tell us that Sudbury has its mind on a future that it is building for itself. An economist can tell you about where the outside world is trying to go. It is really up to you to decide where Sudbury will go in 2009.